A balance sheet is a financial statement that shows the assets, liabilities, and equity of a company or an individual at a specific point in time. It is one of the three main financial statements, along with the income statement and the cash flow statement, that are used to evaluate the financial health and performance of a company or an individual. In this blog post, we will explain what a balance sheet is, what it includes, how to read it, and why it matters for financial decision-making.

What is Included in a Balance Sheet?

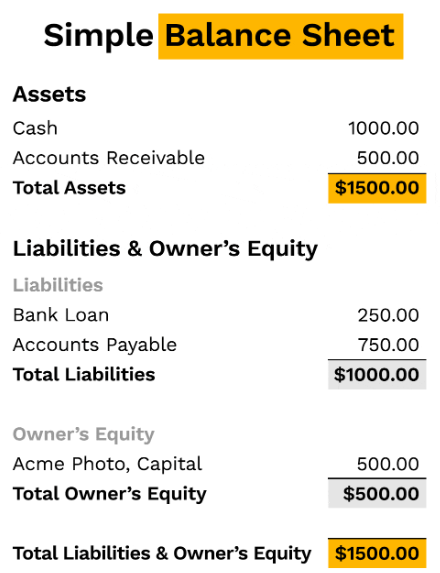

A balance sheet is divided into two sides: the left side lists the assets, and the right side lists the liabilities and the equity. The assets are the resources that the company or the individual owns or controls, such as cash, inventory, property, equipment, investments, etc. The liabilities are the obligations that the company or the individual owes to others, such as loans, accounts payable, taxes, etc. The equity is the difference between the assets and the liabilities, and it represents the ownership interest of the shareholders or the owners in the company or the individual.

The balance sheet follows the basic accounting equation:

Assets=Liabilities+Equity

This means that the total value of the assets must equal the total value of the liabilities and the equity. This equation ensures that the balance sheet is balanced and that the sources of funds (liabilities and equity) match the uses of funds (assets).

The assets and the liabilities are further classified into two categories: current and non-current. Current assets are the assets that are expected to be converted into cash or consumed within one year or the normal operating cycle of the business, whichever is longer. Examples of current assets are cash, accounts receivable, inventory, prepaid expenses, etc. Non-current assets are the assets that are not expected to be converted into cash or consumed within one year or the normal operating cycle of the business, whichever is longer. Examples of non-current assets are property, plant, and equipment, intangible assets, long-term investments, etc.

Current liabilities are the liabilities that are expected to be paid or settled within one year or the normal operating cycle of the business, whichever is longer. Examples of current liabilities are accounts payable, short-term loans, accrued expenses, taxes payable, etc. Non-current liabilities are the liabilities that are not expected to be paid or settled within one year or the normal operating cycle of the business, whichever is longer. Examples of non-current liabilities are long-term loans, bonds payable, deferred taxes, etc.

The equity section of the balance sheet varies depending on the type of the entity. For a corporation, the equity section consists of two main components: share capital and retained earnings. Share capital is the amount of money that the shareholders have invested in the company by buying shares. Retained earnings are the amount of money that the company has earned and retained over time, after paying dividends to the shareholders. For a sole proprietorship or a partnership, the equity section consists of the owner’s or the partners’ capital accounts, which reflect the amount of money that they have invested or withdrawn from the business.

How to Read a Balance Sheet?

A balance sheet provides a snapshot of the financial position of a company or an individual at a given date. It can be used to analyze various aspects of the financial health and performance of the entity, such as liquidity, solvency, efficiency, and profitability. To read a balance sheet, one can use the following steps:

- Identify the type and the date of the balance sheet. The type of the balance sheet indicates the entity that is reporting the financial information, such as a corporation, a sole proprietorship, a partnership, etc. The date of the balance sheet indicates the point in time that the financial information is presented, such as the end of the year, the end of the quarter, etc.

- Examine the assets section of the balance sheet. The assets section shows the resources that the entity owns or controls, and how they are allocated among current and non-current assets. The current assets are listed in the order of liquidity, meaning how easily they can be converted into cash. The non-current assets are listed in the order of permanence, meaning how long they are expected to last. The total assets represent the total value of the resources that the entity has at its disposal.

- Examine the liabilities section of the balance sheet. The liabilities section shows the obligations that the entity owes to others, and how they are allocated among current and non-current liabilities. The current liabilities are listed in the order of maturity, meaning how soon they have to be paid or settled. The non-current liabilities are listed in the order of priority, meaning how senior they are in the event of liquidation. The total liabilities represent the total amount of money that the entity has to pay or settle in the future.

- Examine the equity section of the balance sheet. The equity section shows the ownership interest of the shareholders or the owners in the entity, and how it is composed of share capital and retained earnings (for a corporation) or capital accounts (for a sole proprietorship or a partnership). The total equity represents the residual value of the entity after deducting the liabilities from the assets.

- Compare the balance sheet with the previous periods or the industry averages. By comparing the balance sheet with the previous periods or the industry averages, one can identify the trends and the changes in the financial position of the entity over time or relative to its peers. For example, one can compare the growth or decline of the assets, liabilities, and equity, the composition and the quality of the assets and the liabilities, the liquidity and the solvency ratios, the return on assets and the return on equity, etc.

Why Does a Balance Sheet Matter?

A balance sheet matters for financial decision-making, as it provides valuable information about the financial health and performance of a company or an individual. By reading a balance sheet, one can assess the following aspects of the entity:

- Liquidity: Liquidity is the ability of the entity to meet its short-term obligations with its current assets. A high liquidity indicates that the entity has enough cash or cash equivalents to pay its bills and debts on time. A low liquidity indicates that the entity may face cash flow problems and default on its obligations. Liquidity can be measured by using ratios such as the current ratio, the quick ratio, and the cash ratio.

- Solvency: Solvency is the ability of the entity to meet its long-term obligations with its assets. A high solvency indicates that the entity has enough assets to cover its liabilities and generate income for its owners. A low solvency indicates that the entity may face bankruptcy or insolvency risk and lose its assets to its creditors. Solvency can be measured by using ratios such as the debt-to-equity ratio, the debt-to-assets ratio, and the interest coverage ratio.

- Efficiency: Efficiency is the ability of the entity to use its assets and liabilities effectively and productively. A high efficiency indicates that the entity is generating more revenue and profit with less investment and cost. A low efficiency indicates that the entity is wasting its resources and incurring more expenses. Efficiency can be measured by using ratios such as the asset turnover ratio, the inventory turnover ratio, and the accounts receivable turnover ratio.

- Profitability: Profitability is the ability of the entity to generate income and profit from its operations and investments. A high profitability indicates that the entity is creating value for its owners and shareholders. A low profitability indicates that the entity is losing money and destroying value. Profitability can be measured by using ratios such as the net margin ratio, the return on assets ratio, and the return on equity ratio.

Conclusion

A balance sheet is a financial statement that shows the assets, liabilities, and equity of a company or an individual at a specific point in time. It is based on the accounting equation that states that the assets must equal the liabilities and the equity. A balance sheet can be used to analyze the financial health and performance of the entity, such as liquidity, solvency, efficiency, and profitability. A balance sheet can also be compared with the previous periods or the industry averages to identify the trends and the changes in the financial position of the entity.