Profitability ratios are financial metrics that help investors and analysts assess how well a company can generate income and profit from its operations, assets, and equity. They are useful tools to compare a company’s performance with its peers, industry averages, or historical trends. In this blog, we will explain what profitability ratios are, what are the common types and formulas, and how to interpret and analyze them.

What are Profitability Ratios?

Profitability ratios measure the ability of a company to earn profits from its sales or operations, balance sheet assets, or shareholders’ equity. They indicate how efficiently a company uses its resources to generate value for its owners or shareholders. A higher ratio or value is usually desirable, as it means the company is more profitable and successful at converting revenue to profit. However, profitability ratios should not be viewed in isolation, but rather in conjunction with other financial ratios, such as liquidity ratios, solvency ratios, and efficiency ratios, to get a comprehensive picture of a company’s financial health and performance.

Types and Formulas of Profitability Ratios

There are two main categories of profitability ratios: margin ratios and return ratios. Margin ratios show how much profit a company makes for every dollar of sales, while return ratios show how much profit a company generates for every dollar of investment. Let’s look at some of the most commonly used profitability ratios and their formulas.

Margin Ratios

- Gross Profit Margin: This ratio measures the percentage of revenue that is left after deducting the cost of goods sold (COGS), which are the direct costs of producing or delivering the goods or services. It shows how well a company manages its production or inventory costs and how much it can mark up its products or services. A high gross profit margin indicates a higher efficiency of core operations and a greater potential to cover other expenses and earn net income. The formula for gross profit margin is:

where Gross Profit = Revenue – COGS

- Operating Profit Margin: This ratio measures the percentage of revenue that is left after deducting both the cost of goods sold and the operating expenses, which are the indirect costs of running the business, such as salaries, rent, utilities, marketing, etc. It shows how well a company controls its operating costs and how profitable its core business activities are. A high operating profit margin indicates a higher operational efficiency and a greater ability to withstand changes in sales or costs. The formula for operating profit margin is:

where Operating Profit = Revenue – COGS – Operating Expenses

- Net Profit Margin: This ratio measures the percentage of revenue that is left after deducting all the expenses, including the cost of goods sold, the operating expenses, the interest expenses, the taxes, and any other income or expenses. It shows how much profit a company earns for every dollar of sales after paying all its obligations. It is also known as the bottom line or net income ratio. A high net profit margin indicates a higher overall profitability and a greater return to the owners or shareholders. The formula for net profit margin is:

where Net Profit = Revenue – COGS – Operating Expenses – Interest Expenses – Taxes + Other Income or Expenses

Return Ratios

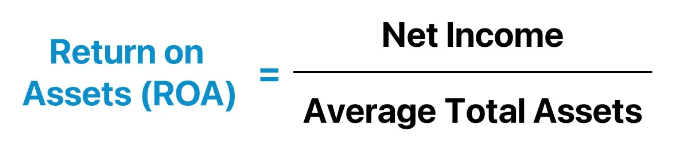

- Return on Assets (ROA): This ratio measures the percentage of profit a company earns for every dollar of assets it owns. Assets are the resources that a company uses to generate income, such as cash, inventory, equipment, property, etc. It shows how efficiently a company utilizes its assets to produce profit and value for shareholders. A high return on assets indicates a higher asset productivity and a greater earning power. The formula for return on assets is:

where Average Total Assets = (Beginning Total Assets + Ending Total Assets) / 2

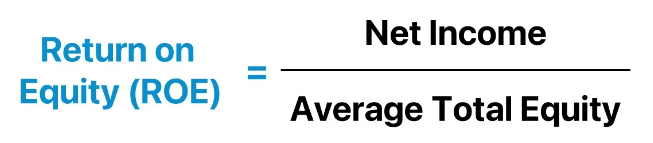

- Return on Equity (ROE): This ratio measures the percentage of profit a company earns for every dollar of equity it has. Equity is the amount of money that the owners or shareholders have invested in the company, or the difference between the total assets and the total liabilities. It shows how effectively a company uses its equity to generate profit and value for shareholders. A high return on equity indicates a higher return on investment and a greater shareholder wealth. The formula for return on equity is:

where Average Shareholders’ Equity = (Beginning Shareholders’ Equity + Ending Shareholders’ Equity) / 2

How to Interpret and Analyze Profitability Ratios

Profitability ratios can provide useful insights into the financial performance and health of a company. However, they should not be used in isolation, but rather in comparison with other relevant information, such as:

- The company’s own historical performance: Comparing the current profitability ratios with the previous periods can reveal the trends and changes in the company’s profitability over time. For example, an increasing gross profit margin may indicate an improvement in production efficiency or pricing strategy, while a decreasing net profit margin may indicate a decline in sales or an increase in costs.

- The industry average or benchmark: Comparing the company’s profitability ratios with the industry average or a similar company can reveal the relative strengths and weaknesses of the company’s profitability in the market. For example, a higher operating profit margin than the industry average may indicate a competitive advantage in cost control or product differentiation, while a lower return on equity than the industry average may indicate a lack of growth opportunities or a high debt burden.

- The company’s goals or expectations: Comparing the company’s profitability ratios with its own goals or expectations can reveal the degree of achievement or deviation of the company’s profitability from its desired level. For example, a higher net profit margin than the expected level may indicate a better than expected performance or a favorable external environment, while a lower return on assets than the expected level may indicate a poor performance or an unfavorable external environment.

Conclusion

Profitability ratios are important financial metrics that help investors and analysts evaluate how well a company can generate income and profit from its operations, assets, and equity. They can also help managers and owners monitor and improve the profitability of their business. By understanding the types, formulas, and interpretations of profitability ratios, you can gain valuable insights into the financial health and performance of a company and make informed decisions.