Stock valuation is the process of estimating the intrinsic or fair value of a stock, based on its expected future performance and cash flows. Stock valuation can help investors and analysts determine whether a stock is overpriced or underpriced in the market, and whether it is a good investment opportunity.

There are two main categories of stock valuation methods: absolute and relative. Absolute valuation methods try to find the true value of a stock based on its own fundamentals, such as earnings, dividends, growth, and risk. Relative valuation methods compare the stock to other similar stocks in the market, and use multiples and ratios, such as the price-to-earnings (P/E) ratio, to measure its value.

In this blog post, we will introduce some of the most common and popular stock valuation methods, and explain how and when to use them.

Absolute Valuation Methods

Absolute valuation methods aim to calculate the present value of the future cash flows that a stock will generate for its shareholders. The most widely used absolute valuation methods are the dividend discount model (DDM) and the discounted cash flow model (DCF).

Dividend Discount Model (DDM)

The dividend discount model (DDM) is based on the assumption that the value of a stock is equal to the present value of its future dividends. The DDM is suitable for valuing stocks that pay stable and predictable dividends, such as mature and stable companies.

The formula for the DDM is:

where:

- PV0 is the current stock price

- D1 is the expected dividend per share in the next period

- r is the required rate of return or the cost of equity

- g is the constant growth rate of dividends

For example, suppose a stock pays an annual dividend of $2 per share, and the dividend is expected to grow at 5% per year. The required rate of return is 10%. The value of the stock using the DDM is:

PV0=42

This means that the stock is worth $42 per share, given the expected dividend, growth rate, and required rate of return.

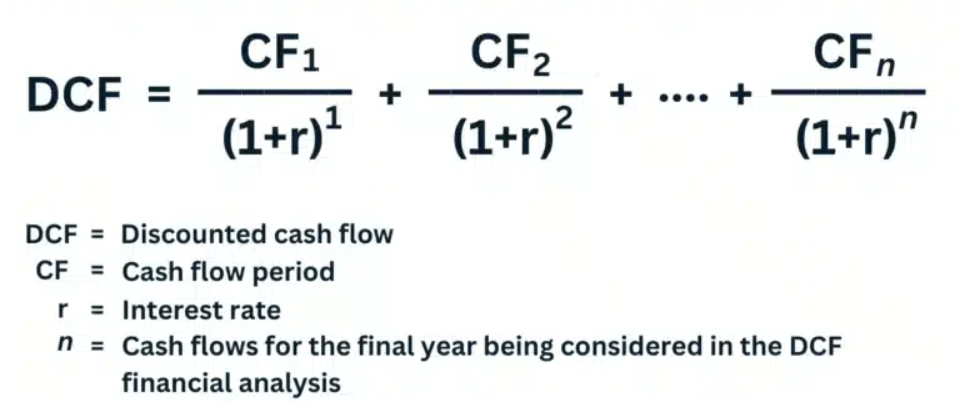

Discounted Cash Flow Model (DCF)

The discounted cash flow model (DCF) is based on the assumption that the value of a stock is equal to the present value of its free cash flows. Free cash flow (FCF) is the cash that a company generates after paying for its operating expenses and capital expenditures. The DCF is suitable for valuing stocks that do not pay dividends, or that have uncertain or irregular dividend payments, such as growth and innovative companies.

The formula for the DCF is:

For example, suppose a stock has the following free cash flows for the next five years, and a terminal value of $100 million. The required rate of return is 12%. The value of the stock using the DCF is:

| Year | FCF ($ million) |

|---|---|

| 1 | 10 |

| 2 | 12 |

| 3 | 15 |

| 4 | 18 |

| 5 | 22 |

P0=8.93+9.57+10.67+11.44+11.12+56.74

P0=108.47

This means that the stock is worth $108.47 million, given the expected free cash flows, terminal value, and required rate of return.

Relative Valuation Methods

Relative valuation methods compare the stock to other similar stocks in the market, and use multiples and ratios to measure its value. The most widely used relative valuation method is the comparable company analysis (CCA).

Comparable Company Analysis (CCA)

The comparable company analysis (CCA) is based on the assumption that the value of a stock is determined by the market forces of supply and demand, and that similar stocks should trade at similar multiples and ratios. The CCA is suitable for valuing stocks that have a lot of peers in the same industry or sector, and that have similar characteristics, such as size, growth, profitability, and risk.

The steps for the CCA are:

- Select a set of comparable companies that are similar to the target company in terms of industry, size, growth, profitability, and risk.

- Calculate the relevant multiples and ratios for each comparable company, such as the P/E ratio, the P/B ratio, the EV/EBITDA ratio, etc.

- Calculate the average or median multiple or ratio for the comparable companies, and apply it to the target company’s financial metrics, such as earnings, book value, EBITDA, etc.

- Adjust the valuation for any differences between the target company and the comparable companies, such as growth prospects, competitive advantages, or risks.

For example, suppose a stock has an earnings per share (EPS) of $2, and we want to value it using the P/E ratio. We select five comparable companies in the same industry, and calculate their P/E ratios as follows:

| Company | EPS | Stock Price | P/E Ratio |

|---|---|---|---|

| A | 1.5 | 30 | 20 |

| B | 2 | 40 | 20 |

| C | 2.5 | 50 | 20 |

| D | 3 | 60 | 20 |

| E | 3.5 | 70 | 20 |

The average P/E ratio for the comparable companies is 20. We apply this multiple to the target company’s EPS of $2, and get a value of $40 per share. However, we notice that the target company has a higher growth rate than the comparable companies, so we adjust the valuation by adding a 10% premium. The final value of the stock using the CCA is $44 per share.

Conclusion

Stock valuation is an essential skill for investors and analysts, as it helps them make informed decisions about buying, selling, or holding a stock. There are many methods of stock valuation, each with its own advantages and disadvantages. The choice of the valuation method depends on the type of stock, the availability of information, and the purpose of the valuation. It is often advisable to use more than one method to cross-check the results and get a more accurate and reliable estimate.