Introduction: The Importance of Personal Finance and Budgeting

In today’s fast-paced world, managing money effectively is crucial to achieving financial freedom and security. Whether you’re a seasoned investor, young professional, or just starting on your financial journey, understanding the basics of personal finance is essential. This includes budgeting—one of the foundational steps in any successful financial plan. A solid budget not only helps you monitor expenses but also ensures that your financial goals remain on track.

In this article, we’ll cover the fundamentals of personal finance, including budgeting basics, strategies for success, and how these practices can positively impact your financial well-being.

What is Personal Finance?

Personal finance refers to the management of one’s financial activities, including income, expenses, savings, investments, and debt management. Understanding personal finance allows individuals to make informed decisions about their money, helping to meet both short-term needs and long-term goals.

Why Personal Finance Matters

Personal finance skills are essential to:

- Achieve financial independence.

- Build an emergency fund for unforeseen expenses.

- Make sound investment decisions.

- Plan for retirement and other future goals.

Building a strong foundation in personal finance empowers you to control your financial future, avoid debt, and create a path toward long-term wealth.

The Basics of Personal Finance

Starting with the basics of personal finance is essential to building a solid financial foundation. Here are some core concepts:

1. Income Management

Understanding and tracking your income is the first step. This includes any wages, salaries, investments, or other sources of earnings. Knowing how much money you have to work with each month sets the stage for effective budgeting.

2. Expense Tracking

Keeping track of expenses helps identify spending habits and areas where you might be able to save. Separate expenses into fixed (e.g., rent, utilities) and variable (e.g., entertainment, dining out) categories to see where adjustments can be made.

3. Saving and Investing

Saving should be prioritized to build an emergency fund and meet future needs. Investing, on the other hand, helps grow your wealth over time. Both savings and investments are crucial to achieving financial goals, from buying a home to retiring comfortably.

4. Debt Management

Not all debt is negative, but it’s essential to manage it wisely. High-interest debt, such as credit card debt, can become a financial burden if not paid off promptly. Focus on paying down high-interest debt first, and avoid taking on unnecessary loans.

Budgeting: The Foundation of Financial Success

Budgeting is the practice of creating a plan to spend your money. This financial roadmap ensures that you don’t overspend and helps you reach your financial goals. Budgeting is especially useful for beginners learning to manage their finances but is also beneficial for anyone looking to refine their financial habits.

Benefits of Budgeting

- Keeps spending under control.

- Helps achieve short-term and long-term financial goals.

- Builds a habit of saving and reduces stress over money.

- Allows you to allocate funds for investments and retirement.

Types of Budgeting Methods

1. Zero-Based Budgeting

With zero-based budgeting, every dollar has a purpose. This method involves allocating every dollar of income to specific expenses, savings, or debt payments, resulting in a zero balance by the end of the month. It’s ideal for those who want detailed control over their finances.

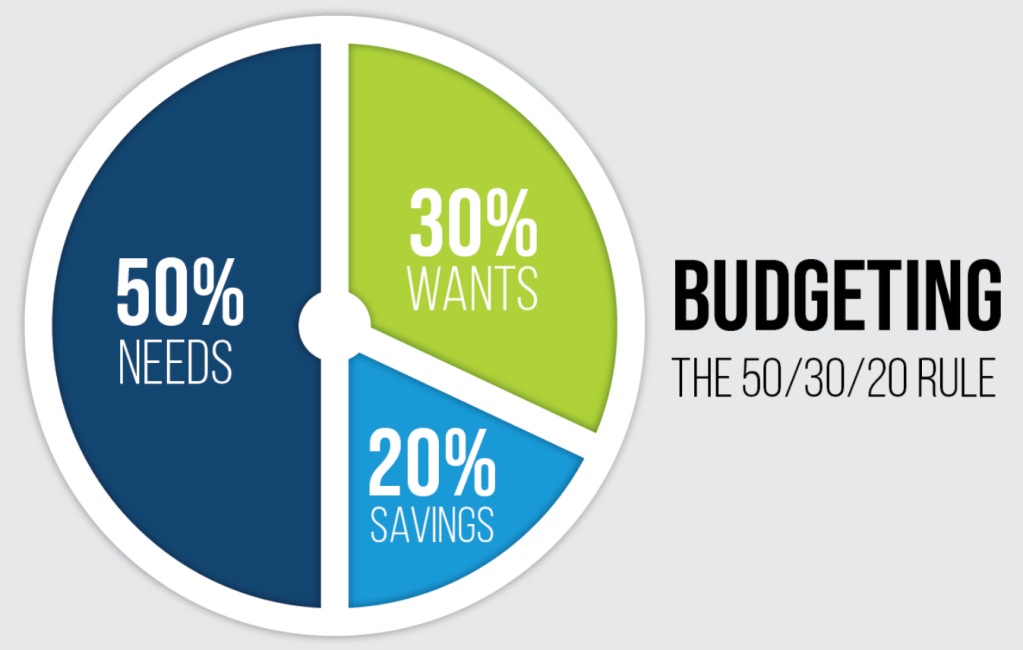

2. 50/30/20 Rule

The 50/30/20 rule is a straightforward budgeting method that allocates:

- 50% of income for necessities (rent, groceries).

- 30% for discretionary spending (entertainment).

- 20% for savings and debt repayment.

This method is particularly useful for beginners because it provides flexibility while still prioritizing saving.

3. Envelope System

This system involves placing cash in envelopes for each spending category, such as groceries, entertainment, and utilities. Once an envelope is empty, spending in that category stops until the next budget period. The envelope system is a practical way to curb overspending.

Creating a Personal Budget: Step-by-Step Guide

Step 1: Calculate Monthly Income

Include all sources of income, such as salaries, freelance earnings, or investment dividends. Knowing your total income gives you a realistic picture of your monthly spending limit.

Step 2: List All Expenses

Identify all expenses, including fixed costs (like rent and utilities) and variable costs (such as groceries and entertainment). This step reveals your current spending habits and shows where cuts might be made.

Step 3: Set Financial Goals

Define clear financial goals, both short-term and long-term. Short-term goals might include building an emergency fund, while long-term goals could involve buying a home or saving for retirement.

Step 4: Create Spending Limits

Assign spending limits to each category based on your income and financial goals. This step is crucial for maintaining balance and preventing unnecessary expenditures.

Step 5: Track and Adjust Monthly

Monitor your budget regularly and make adjustments as needed. You may find certain areas where you can cut back to save more toward your goals.

Overcoming Common Budgeting Challenges

Despite its importance, budgeting can be challenging. Here are some common obstacles and tips to overcome them:

Lack of Discipline

Sticking to a budget requires discipline. To stay motivated, remind yourself of the benefits and track your progress toward your financial goals.

Overspending on Discretionary Items

Discretionary spending is often the main culprit for budget issues. Consider limiting discretionary categories and setting aside a set amount for fun and leisure.

Irregular Income

If you have irregular income, such as from freelance work, base your budget on the average of your last few months’ income. Prioritize saving during high-income months to balance out low-income periods.

Conclusion: Take Control of Your Financial Future with Budgeting

Mastering personal finance starts with budgeting, the cornerstone of any successful financial plan. By understanding and managing your income, expenses, and savings, you can take control of your finances and achieve long-term stability. Whether you’re a student, a young professional, or simply looking to improve your financial habits, effective budgeting can pave the way to financial freedom.

Budgeting and personal finance basics are not just for experts; they are essential skills for everyone. By taking small steps today, you’re investing in a more secure, financially sound future for tomorrow.