As we approach the end of 2024 and look toward the opportunities awaiting in 2025, many middle-aged adults are re-evaluating their financial goals, particularly around Retirement. Navigating the complexities of pensions, savings, and investments can be challenging—especially in today’s rapidly changing economic environment. However, crafting a Retirement Strategy doesn’t have to be overwhelming. With the right guidance, you can make informed decisions to safeguard your future and enter your golden years with confidence.

This article will explore practical steps you can take to close out 2024 on a strong note and kickstart 2025 with a well-rounded approach to Retirement Strategy. From evaluating your current savings to capitalizing on employer-sponsored plans and understanding healthcare costs, we’ll cover key considerations that can help you build lasting financial security. Whether you’re new to the idea of structured planning or looking to refine an existing blueprint, these insights will help you retire in comfort and peace.

Assessing Your Financial Landscape

Taking Stock of Your Current Position

Before diving deeper into the various aspects of your Retirement plan, take the time to assess your current financial standing. Gather information about your monthly income, living expenses, outstanding debts, and existing retirement accounts. If you have a partner or spouse, include their financial information as well so you both have a clear, shared view of the household balance sheet.

- Income Sources: Identify your main and supplementary sources of income, such as salaries, rental income, or freelance work.

- Expenses: Categorize your expenses into needs (housing, utilities, food) and wants (entertainment, luxury items). This helps you see where you could potentially cut back to channel more funds into your Retirement Strategy.

- Debts: Note credit card balances, mortgages, personal loans, or any other financial obligations. Prioritize paying down high-interest debts to free up extra cash.

By establishing a comprehensive overview of your finances, you’ll lay the groundwork for a more targeted approach as we move into 2025. This clarity can also help you identify gaps—areas where you might need to adjust contributions to your Retirement accounts or explore new investment opportunities.

Evaluating Your Retirement Accounts

Many people have multiple Retirement accounts—like 401(k)s, IRAs, or pension funds—often from different jobs or financial institutions. Conduct a detailed review:

- Contributions: Are you contributing enough to get the full employer match on a 401(k)? If not, consider increasing your contributions to avoid leaving “free money” on the table.

- Asset Allocation: Look at the mix of stocks, bonds, and other assets in each of your Retirement accounts. As a middle-aged investor, balancing growth and stability becomes increasingly important.

- Fees and Expenses: Some funds charge higher fees than others, which can erode your returns over time. Investigate whether lower-cost options are available and align with your goals.

Analyzing each account will give you a clearer picture of how effectively your money is working for you and whether you need to adjust your approach heading into 2025.

Refining Your Retirement Strategy

Setting Realistic Goals for 2025 and Beyond

Every solid Retirement Strategy starts with a clear set of objectives. As you approach 2025, define both short-term and long-term goals:

- Short-Term Objectives (6-12 Months): Perhaps you aim to reduce high-interest credit card debt, build an emergency fund covering three to six months of expenses, or slightly increase your monthly contribution to a Retirement account.

- Long-Term Objectives (5-15 Years): These might involve fully paying off a mortgage before you stop working, accumulating a certain net worth by retirement age, or relocating to an area with a lower cost of living.

Balancing near-term and distant goals ensures you’re both able to weather unexpected financial hiccups in 2025 and remain on track toward your ideal Retirement scenario.

Risk Tolerance and Asset Allocation

The economic climate can fluctuate, but a prudent Retirement Strategy often involves maintaining a balanced portfolio. In your middle years, you’re likely aiming to grow your nest egg while preserving capital for the not-so-distant future:

- Growth vs. Stability: If you’re comfortable with some risk, you might allocate a portion of your investments to equities (stocks) for higher growth potential. However, you may also want to hold steady assets (like bonds or stable value funds) for more predictable returns.

- Diversification: Spreading your investments across various sectors—technology, healthcare, consumer goods—can help mitigate losses if one area experiences a downturn.

- Regular Rebalancing: Your asset allocation may drift over time due to market movements. Commit to reviewing your portfolio at least annually, adjusting as needed to maintain your target allocation.

Remember, the right balance will differ from person to person. Speak with a financial advisor or use online risk-assessment tools to gauge whether your Retirement accounts align with your comfort level and future ambitions.

Healthcare Considerations and Insurance

Planning for Medical Expenses

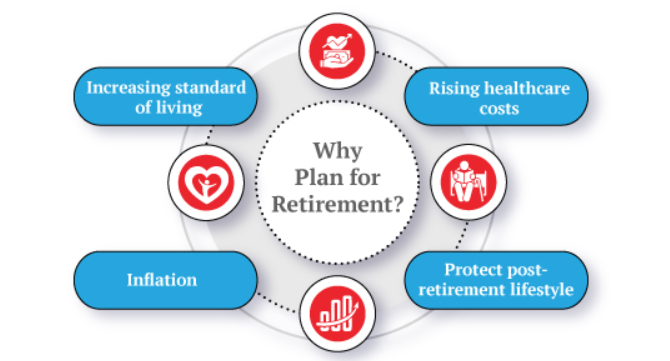

As you plan your Retirement Strategy, don’t overlook healthcare costs. According to various studies, retirees in developed countries often spend a considerable portion of their income on medical care. While the exact amount varies by location and personal health status, you can prepare by:

- Investigating Health Savings Accounts (HSAs): If your health insurance plan qualifies, contributing to an HSA can yield significant tax advantages and help you build a cushion for future medical expenses.

- Estimating Long-Term Care Costs: Nursing homes, in-home care, or assisted living can become necessary later in life. Consider insurance products designed to offset these costs or earmark a portion of your investments to cover potential care needs.

Insurance as a Safety Net

Health insurance and life insurance can serve as additional pillars of a robust Retirement Strategy. As you get older, premiums for life insurance policies can rise, so it’s wise to evaluate whether your current coverage is sufficient. Think about factors like mortgage debt, dependents’ needs, and final expenses when deciding on coverage levels.

Maximizing Income Streams

Delaying Retirement or Working Part-Time

For many in their 40s or 50s, the idea of an immediate transition to full Retirement is evolving. Some prefer a phased approach. You might reduce your work hours or shift to part-time roles, allowing you to maintain a sense of structure and a continuing income stream. This strategy can:

- Reduce Withdrawals: Earning even a modest wage in your early retirement years can let you keep more money invested, potentially extending the life of your nest egg.

- Boost Social Connections: Remaining in the workforce (in some capacity) can also foster community engagement, which contributes to emotional well-being.

Diversifying Income Beyond the Day Job

Even if you decide to exit full-time work, you could explore supplemental income strategies. Some examples:

- Rent Out a Room or Property: If you own property, consider short-term rentals or hosting travelers for additional monthly cash flow.

- Consulting and Freelancing: Transform your professional expertise into a flexible, project-based income.

- Investing in Dividend-Paying Stocks: While no investment is guaranteed, many stable companies offer regular dividend payments. Over time, these can become a reliable source of passive income.

In all these scenarios, weigh the effort and risk involved before finalizing your approach, ensuring it aligns with your broader Retirement Strategy.

Navigating Tax Implications

Timing of Withdrawals

Taxes can significantly impact the funds you have available in Retirement. If you’re close to retirement age, you might be strategizing around traditional IRA or 401(k) distributions, which are typically taxed upon withdrawal. Roth accounts, in contrast, can often be accessed tax-free. The timing and sequence of these distributions may influence your tax bracket from year to year.

- Required Minimum Distributions (RMDs): Traditional IRAs and most employer-sponsored retirement plans require RMDs starting at a certain age (often 73 or older, depending on current regulations). Neglecting RMDs can lead to penalties.

- Roth Conversions: If you expect to be in a higher tax bracket later, converting some funds from a traditional account to a Roth account could reduce your future tax liability. Weigh this carefully, as conversions trigger taxes on the converted amount.

Capital Gains and Estate Considerations

Those holding significant assets outside of qualified Retirement accounts—like real estate or stocks in a brokerage account—should keep capital gains taxes on their radar. Selling an appreciated property or stock can lead to a hefty tax bill, which may reduce the funds you’ve earmarked for your Retirement Strategy.

Estate taxes are another consideration for those with large estates. Although thresholds for estate taxes in developed countries can be relatively high, it’s prudent to consult with a tax professional to ensure your future legacy is passed on efficiently to heirs or charities.

Conclusion

Closing out 2024 and entering 2025 with a well-defined Retirement Strategy can set the stage for a more secure and fulfilling next chapter of your life. By assessing your current finances, refining asset allocations, considering healthcare expenses, and planning for potential tax implications, you’ll build a robust foundation that can withstand market changes and personal life transitions.

Action Steps to Strengthen Your Retirement Today:

- Conduct a Thorough Financial Review: Gather statements, list out debts, and scrutinize your Retirement accounts to see where you stand.

- Clarify Your Goals: Identify what you want from your retirement years—whether it’s traveling the world, spending time with family, or continuing to work part-time for personal satisfaction.

- Explore Supplemental Income: If you foresee any shortfall, think about how freelancing, consulting, or investing in dividend-paying stocks could help bridge the gap.

- Seek Professional Advice: Tax laws, estate planning, and healthcare can be complex. Consulting a financial planner or tax professional may save you money and headaches in the long run.

Staying proactive, informed, and open to adjusting your Retirement Strategy is vital for middle-aged adults in developed countries looking to retire comfortably. Small improvements in how you save or invest can yield substantial benefits over time. Begin implementing changes today, and you’ll enter 2025 with newfound confidence, knowing that each decision brings you closer to a well-earned, secure, and fulfilling Retirement.